Mutual Fund Risk Ratios | What are Alpha Beta Standard Deviation Sharpe Ratio

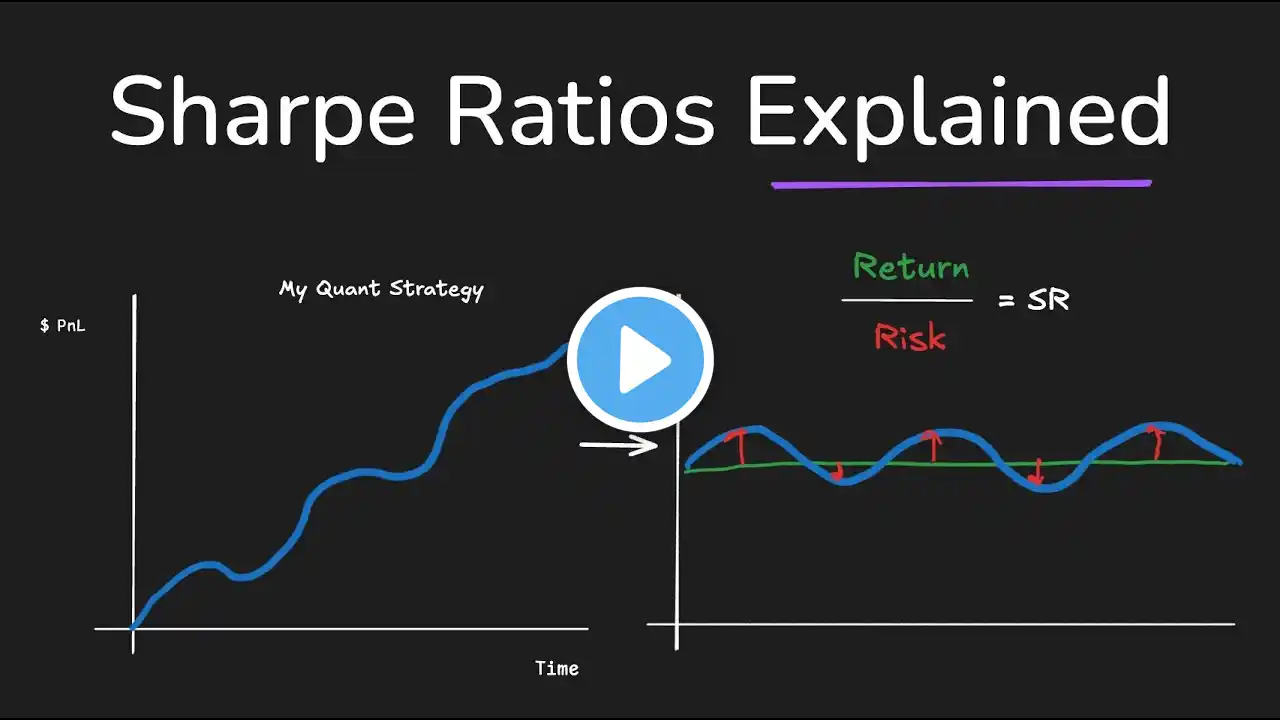

A mutual fund risk ratio is a financial measurement used to assess the level of risk associated with a mutual fund investment. It helps investors to evaluate the potential volatility and stability of a mutual fund before making an investment decision. The mutual fund risk ratio is calculated using a range of statistical measures such as standard deviation, beta, and alpha. The standard deviation measures the variability of the returns of a mutual fund over a given period of time. Beta measures the correlation of a mutual fund's returns with those of the market, and alpha measures the mutual fund's performance compared to its benchmark index. A high mutual fund risk ratio suggests that the investment is more volatile and may experience larger fluctuations in returns over time. Conversely, a low mutual fund risk ratio indicates that the investment is less volatile and may offer more stable returns. Investors should carefully consider a mutual fund's risk ratio before investing in it, as higher-risk investments may offer higher potential returns but also come with a greater chance of losses. In general, investors should seek a balance between risk and return that aligns with their investment goals and risk tolerance. Mutual Fund Risk Ratios | What are Alpha Beta Standard Deviation Sharpe Ratio #mutualfunds