What is Sharpe Ratio? | Definition of Sharpe Ratio | Mutual Fund Risk Ratios

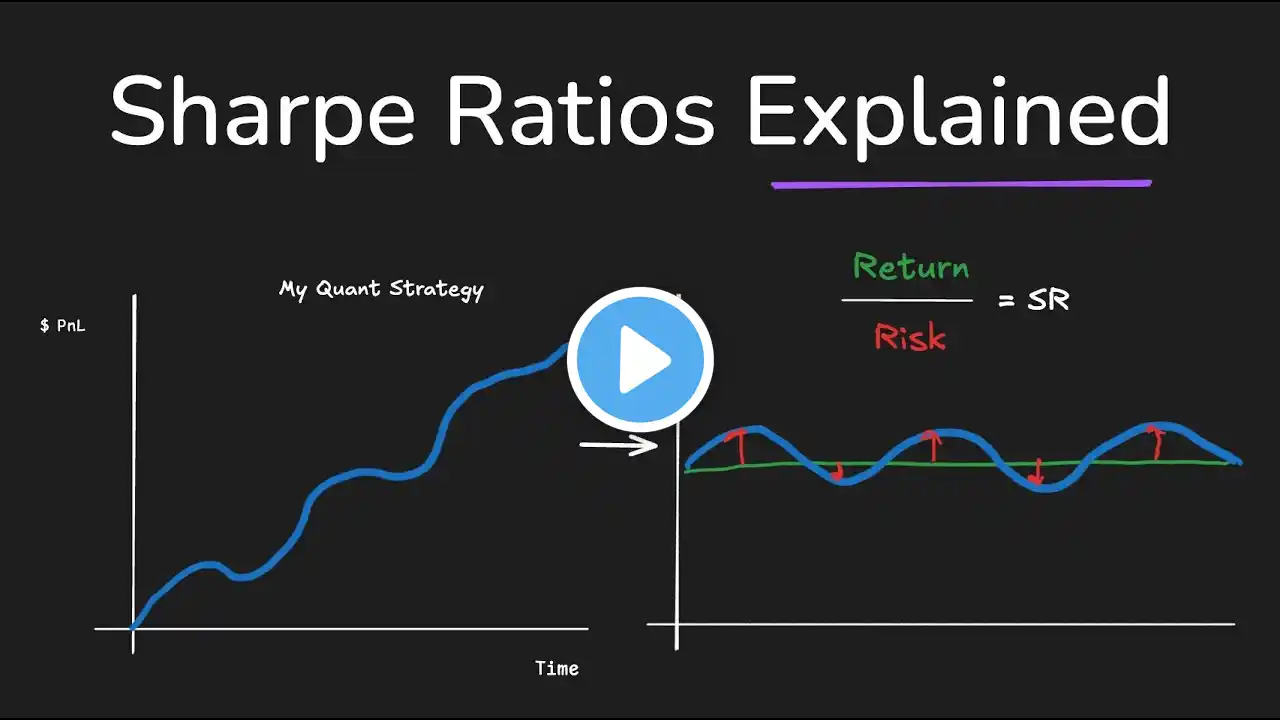

#sharperatio #mutualfunds #investyadnya #yia Sharpe ratio is a measure of excess portfolio return over the risk-free rate relative to its standard deviation. If two funds offer similar returns, the one with a higher standard deviation will have a lower Sharpe ratio. In order to compensate for the higher standard deviation, the fund needs to generate a higher return to maintain a higher Sharpe ratio. In simple terms, it shows how much additional return an investor earns by taking additional risk. Intuitively, it can be inferred that the Sharpe ratio of a risk-free asset is zero. Find us on Social Media and stay connected: Facebook Page - / investyadnya Facebook Group - https://goo.gl/y57Qcr Twitter - / investyadnya