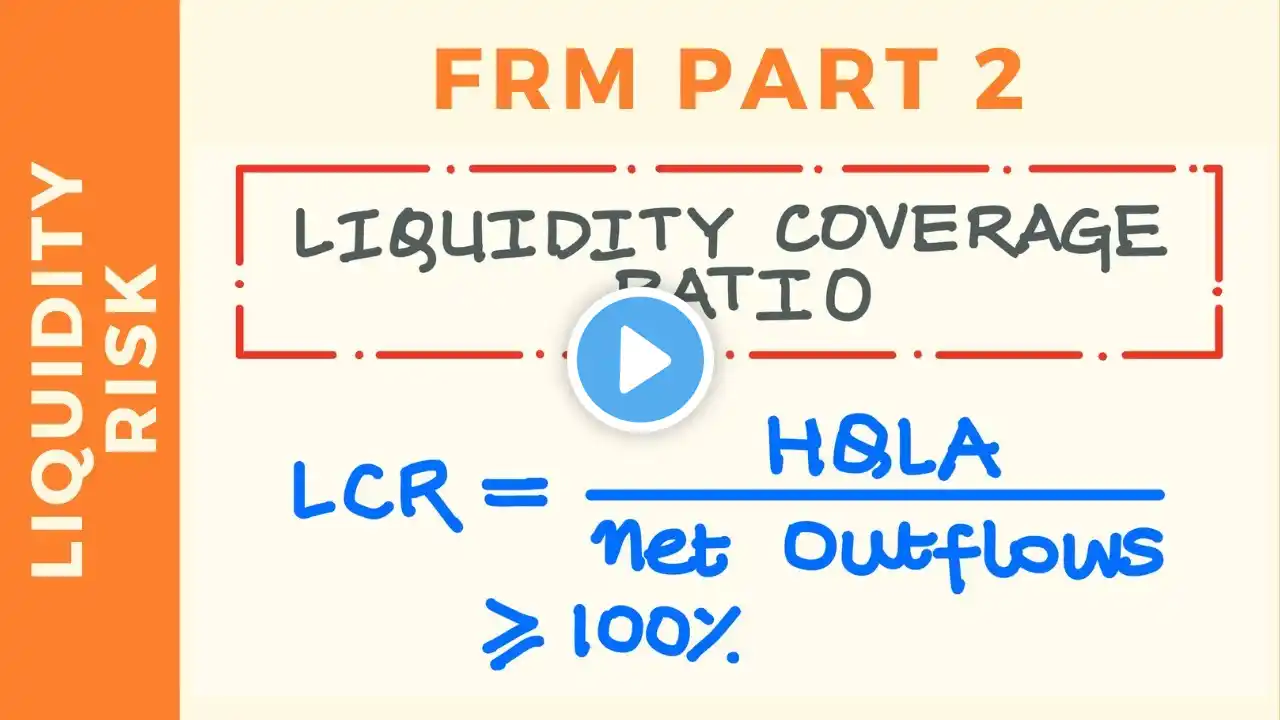

Liquidity coverage ratio (LCR) explained: Measuring liquidity risk (Excel)

How is liquidity risk measured in banks under Basel III? What are the regulatory requirements? And how one can calculate these metrics without access to internal bank data? Today we are discussing the liquidity coverage ratio - a measure of short-term liquidity under stress - and its calculation on a real-world example from publicly available data, making sense of the methodology and discussing its advantages and limitations. Don't forget to subscribe to NEDL and give this video a thumbs up for more videos in Finance! Please consider supporting NEDL on Patreon: / nedleducation