SA 701 - Key Audit Matters (KAM)- CA Final, CA Inter, CA IPCC

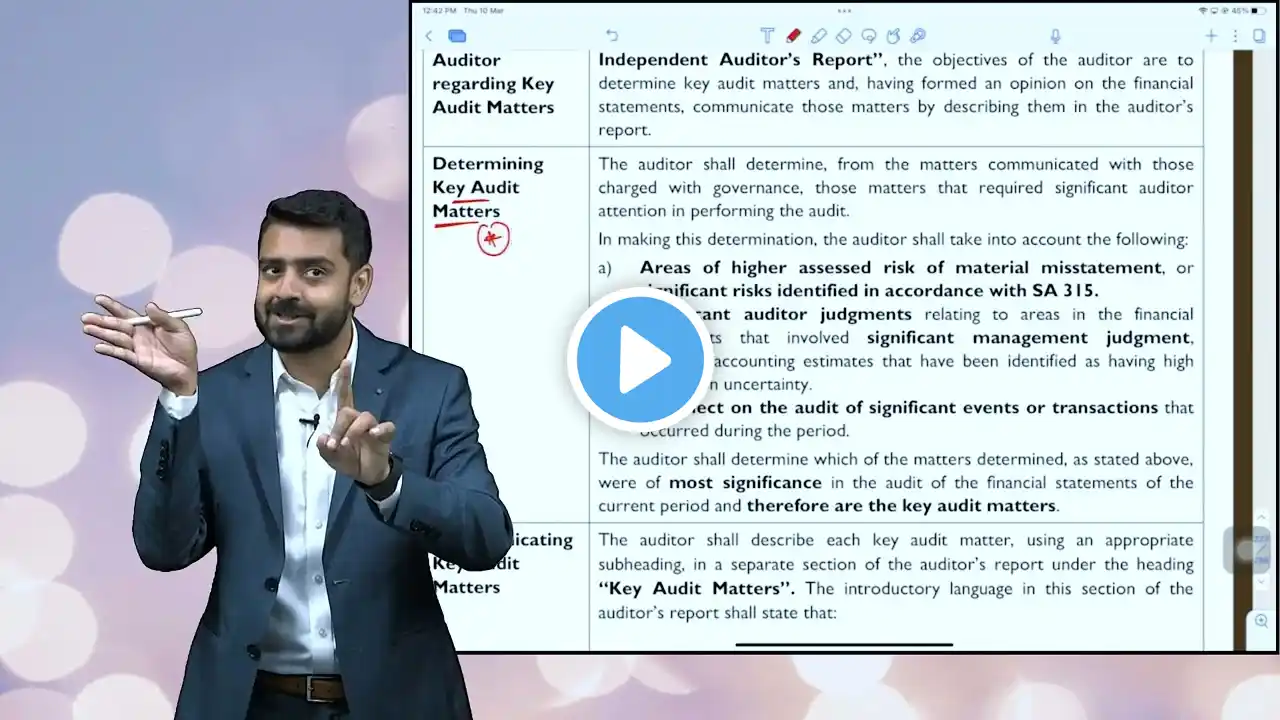

Communicating key audit matters in the auditor’s report is in the context of the auditor having formed an opinion on the financial statements as a whole. Communicating key audit matters in the auditor’s report is not: (a) A substitute for disclosures in the financial statements that the applicable financial reporting framework requires management to make, or that are otherwise necessary to achieve fair presentation; (b) A substitute for the auditor expressing a modified opinion when required by the circumstances of a specific audit engagement in accordance with SA 705 (Revised);1 (c) A substitute for reporting in accordance with SA 570 (Revised)2 when a material uncertainty exists relating to events or conditions that may cast significant doubt on an entity’s ability to continue as a going concern; or (d) A separate opinion on individual matters. Determining Key Audit Matters 9. The auditor shall determine, from the matters communicated with those charged with governance, those matters that required significant auditor attention in performing the audit. In making this determination, the auditor shall take into account the following: (Ref: Para. A9–A18) (a) Areas of higher assessed risk of material misstatement, or significant risks identified in accordance with SA 315.5 (Ref: Para. A19–A22) (b) Significant auditor judgments relating to areas in the financial statements that involved significant management judgment, including accounting estimates that have been identified as having high estimation uncertainty. ) (c) The effect on the audit of significant events or transactions that occurred during the period. 10. The auditor shall determine which of the matters determined in accordance with paragraph 9 were of most significance in the audit of the financial statements of the current period and therefore are the key audit matters. Communicating Key Audit Matters 11. The auditor shall describe each key audit matter, using an appropriate subheading, in a separate section of the auditor’s report under the heading “Key Audit Matters,” unless the circumstances in paragraphs 14 or 15 apply. The introductory language in this section of the auditor’s report shall state that: (a) Key audit matters are those matters that, in the auditor’s professional judgment, were of most significance in the audit of the financial statements of the current period]; and (b) These matters were addressed in the context of the audit of the financial statements as a whole, and in forming the auditor’s opinion thereon, and the auditor does not provide a separate opinion on these matters. (Ref: Para. A31–A33) Key Audit Matters Not a Substitute for Expressing a Modified Opinion 12. The auditor shall not communicate a matter in the Key Audit Matters section of the auditor’s report when the auditor would be required to modify the opinion in accordance with SA 705 (Revised) as a result of the matter. (Ref: Para. A5) Descriptions of Individual Key Audit Matters 13. The description of each key audit matter in the Key Audit Matters section of the auditor’s report shall include a reference to the related disclosure(s), if any, in the financial statements and shall address: (a) Why the matter was considered to be one of most significance in the audit and therefore determined to be a key audit matter; and (Ref: Para. A42–A45) (b) How the matter was addressed in the audit.