Difference between capital expenditure and revenue expenditure in Urdu and Hindi

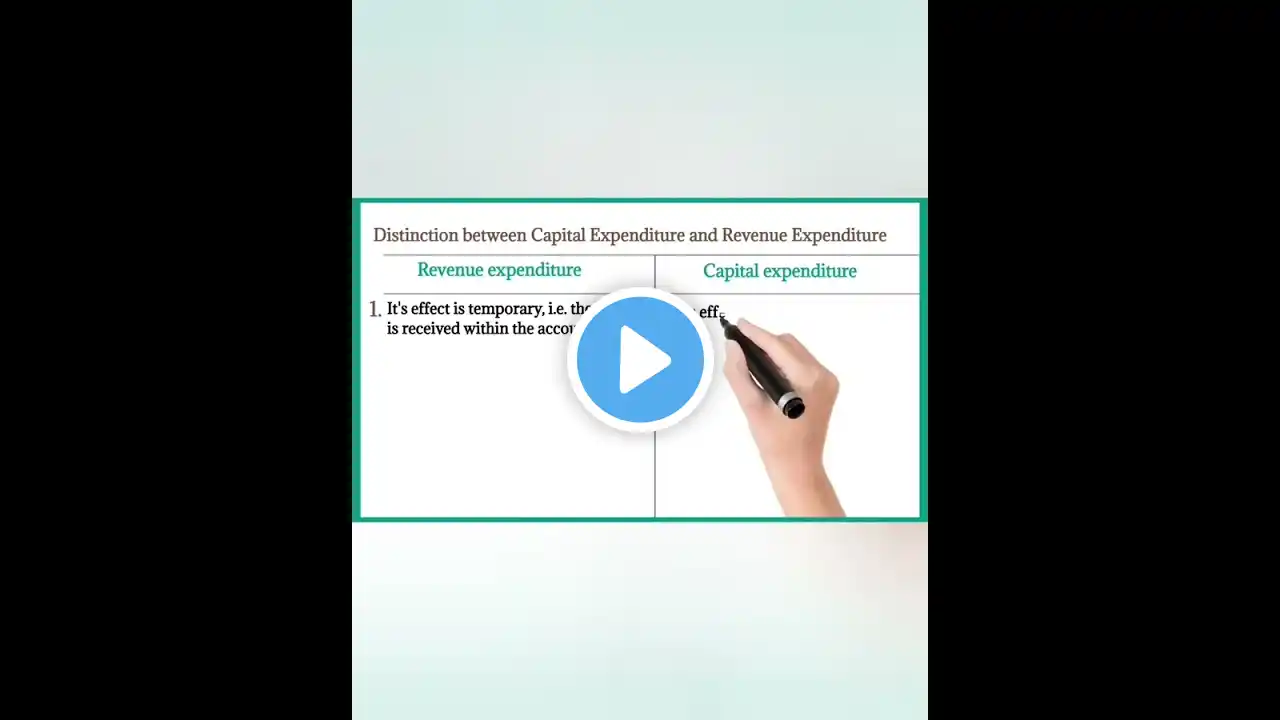

Capital expenditure and revenue expenditure are two distinct types of expenses incurred by a business or organization. The main difference between them lies in their purpose and impact on the financial statements. Here's a breakdown of each: Capital Expenditure: Definition: Capital expenditure (CapEx) refers to the funds spent on acquiring, improving, or extending a long-term asset that will generate benefits beyond the current accounting period. Purpose: CapEx is incurred to enhance the earning capacity or efficiency of a business and to increase its long-term productive capacity. It involves investments in assets such as property, plant, equipment, vehicles, machinery, or technology infrastructure. Treatment: Capital expenditures are considered as investments and are recorded as assets on the balance sheet. These assets are subject to depreciation or amortization over their useful lives. The related costs are allocated over multiple accounting periods to match the benefits derived from the expenditure. Example: Purchasing a new manufacturing plant, acquiring a delivery truck, or upgrading computer systems are examples of capital expenditures. Revenue Expenditure: Definition: Revenue expenditure (RevEx) refers to the funds spent on the day-to-day operational expenses required to maintain the normal functioning of a business or organization. Purpose: RevEx is incurred to sustain the existing operations, maintain assets, and generate immediate benefits within the current accounting period. It includes expenses such as wages, rent, utilities, repairs, advertising, and inventory purchases. Treatment: Revenue expenditures are considered as expenses and are recorded on the income statement. They are deducted from revenues during the same accounting period to determine the net profit or loss. Revenue expenditures do not result in the creation of new assets or an increase in productive capacity. Example: Paying employee salaries, utility bills, or advertising expenses are examples of revenue expenditures. In summary, capital expenditures are long-term investments made to acquire or improve assets that provide lasting benefits, while revenue expenditures are day-to-day operational expenses incurred to maintain the ongoing business activities.